The Hidden Cost of Waiting: How Delaying Bankruptcy Filing Destroys Recovery Chances

The phone rings at 2 AM with another collection call. You've already drained your retirement account and borrowed against your home. Each month brings deeper financial quicksand. Yet you delay filing bankruptcy, hoping something will change.

That hesitation carries hidden costs that bankruptcy attorneys witness constantly. Assets that could have been protected get seized. Retirement funds that were exempt get spent. Options that existed six months ago disappear entirely.

Understanding the precise costs of delay transforms vague anxiety into concrete decision-making. This analysis reveals exactly what waiting costs and why earlier filing typically produces better outcomes.

Cost of Delay Timeline

| Delay Period | Common Losses | Recovery Impact |

|---|---|---|

| 1-3 months | Emergency fund depletion | Minimal cushion for restart |

| 3-6 months | Retirement account raids | Decade of lost growth |

| 6-12 months | Home equity exhausted | Housing stability lost |

| 12-24 months | Judgments and liens | Complex legal untangling |

| 24+ months | Complete asset erosion | Starting from zero |

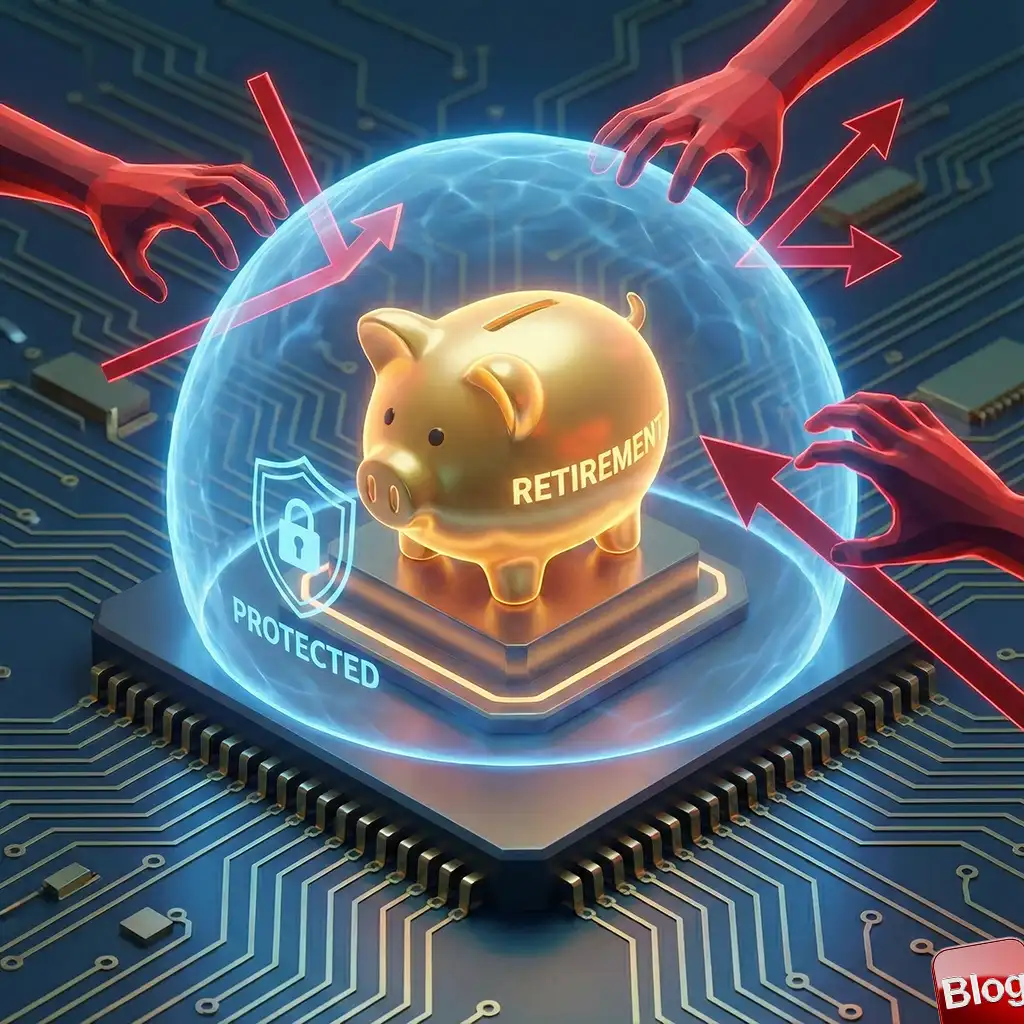

The Retirement Account Trap

ERISA-qualified retirement accounts receive absolute protection in bankruptcy. Your 401(k), traditional IRA, Roth IRA, and pension benefits cannot be touched by creditors or bankruptcy trustees. That $200,000 sitting in your retirement account stays yours completely—if you file bankruptcy with it still intact.

The tragedy bankruptcy attorneys witness repeatedly involves debtors who drain protected retirement accounts to pay unsecured debts. Credit card companies, medical creditors, and personal loan holders receive money they would have gotten zero of in bankruptcy. The debtor exchanges protected assets for temporary relief that ultimately changes nothing about their financial trajectory.

Consider a 45-year-old with $150,000 in retirement savings and $80,000 in credit card debt. If they file bankruptcy immediately, they keep all $150,000 and discharge the $80,000. If they wait, spending $50,000 from retirement to make minimum payments for two years before finally filing, they emerge from bankruptcy with $100,000 less in retirement savings—money that would have grown to over $400,000 by age 65.

The math devastates long-term wealth. Early withdrawal penalties consume 10% immediately. Income taxes take another 20-35%. That $50,000 withdrawal might net only $30,000 after penalties and taxes. Then compound growth losses multiply the damage across decades. Delaying bankruptcy to raid retirement accounts represents perhaps the single most financially destructive decision struggling debtors make.

Other Protected Assets at Risk

Retirement accounts aren't the only protected assets debtors sacrifice while delaying. Most states protect significant home equity through homestead exemptions. Some protect vehicles up to certain values. Personal property exemptions cover household goods, clothing, and necessary items. Life insurance policies with cash value often receive protection as well.

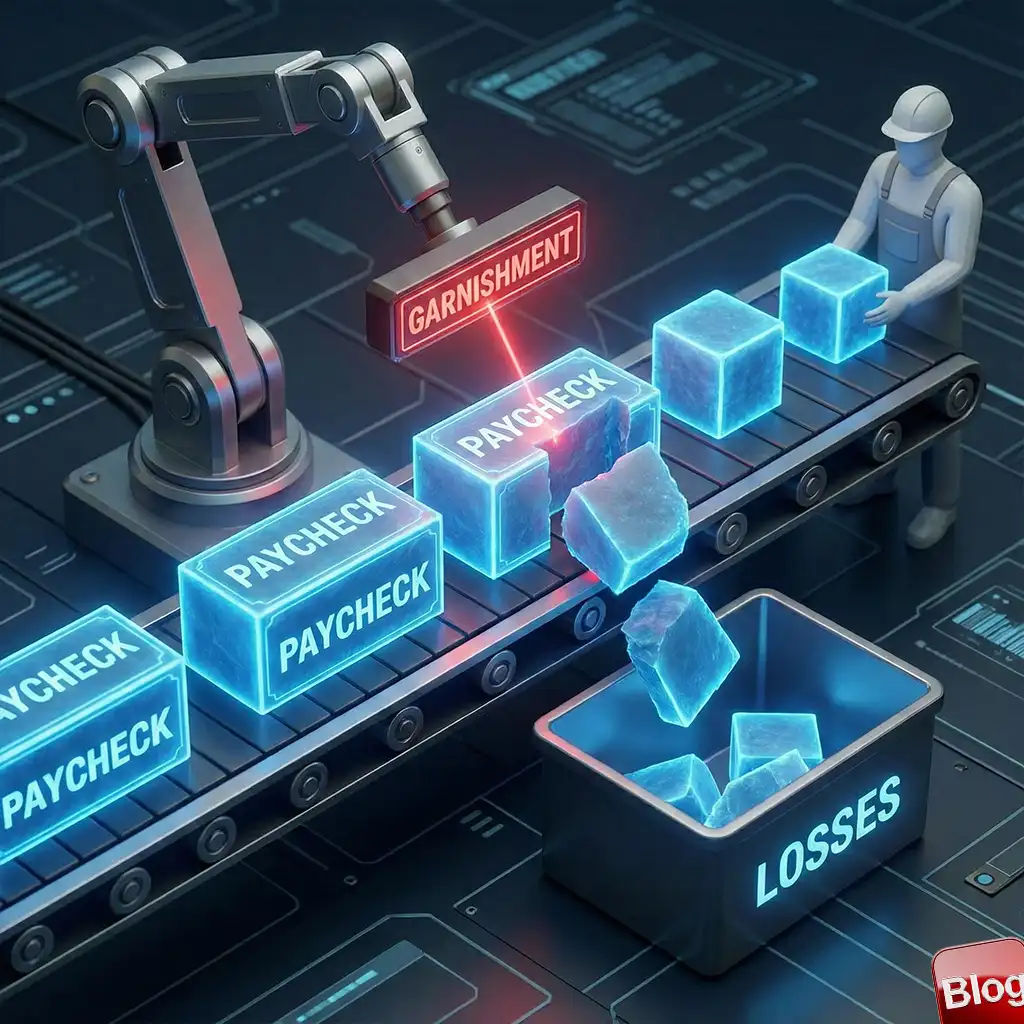

Wage Garnishment Acceleration

Creditors who obtain judgments can garnish wages in most states—typically up to 25% of disposable income. Once garnishment begins, the money disappears from paychecks before you see it. Filing bankruptcy stops garnishment immediately through the automatic stay, but money already taken rarely comes back.

The delay calculation becomes painfully concrete with garnishment. A debtor earning $60,000 annually might lose $15,000 per year to wage garnishment—$1,250 monthly. Every month of delay costs $1,250 that could have stayed in the debtor's pocket if bankruptcy had been filed earlier. Over a year, that's real money that supported the creditor rather than the debtor's fresh start.

Some debtors hope to satisfy the judgment through garnishment, avoiding bankruptcy entirely. This rarely works financially. Interest continues accruing on the judgment. The underlying debt problems that created the initial default remain unaddressed. Meanwhile, the debtor lives on 75% of their income indefinitely, unable to build savings or address other financial needs.

Bank account levies represent another immediate threat. Once a creditor obtains a judgment, they can instruct the sheriff to seize funds directly from your bank accounts. One morning you check your balance and discover it's zero—every dollar taken to satisfy a judgment. The money you needed for rent, groceries, and utilities is gone. Bankruptcy would have stopped this levy, but only if filed before the seizure occurred.

The Lawsuit Avalanche Effect

Creditors don't sue immediately when accounts default. Collection calls come first, then letters, then threats. Actual lawsuits follow months later. But once one creditor files suit, others notice. Credit reports show the lawsuit. Other creditors realize the debtor is vulnerable and accelerate their own collection efforts.

This avalanche effect transforms manageable debt problems into legal nightmares. A debtor facing one lawsuit might handle it. A debtor facing seven simultaneous lawsuits needs an attorney for each case, must respond to multiple court deadlines, and watches judgments accumulate rapidly. Each judgment creates a lien. Each lien complicates property ownership. Each complication requires legal work to untangle.

Consequences of allowing lawsuits to accumulate before filing:

- Multiple judgment liens attach to real property, requiring adversary proceedings to remove even after discharge

- Bank accounts may be levied multiple times by different judgment creditors before bankruptcy protection kicks in

- Legal fees multiply as each case requires separate attention from bankruptcy counsel during case preparation

- Asset seizures may occur before bankruptcy filing, requiring complex recovery efforts or complete loss of property

The Preference Payment Problem

Debtors who delay filing often make the situation worse by paying some creditors while ignoring others. These preference payments create complications in bankruptcy. The trustee can potentially recover payments exceeding $600 made to creditors within 90 days before filing—or one year for payments to insiders like family members.

A debtor who pays mom back $10,000 for a personal loan eight months before filing bankruptcy watches the trustee sue mom to recover that money. The payment was a preference. Mom must return it to the bankruptcy estate for distribution among all creditors. Family relationships strain under such circumstances, creating emotional costs beyond the financial ones.

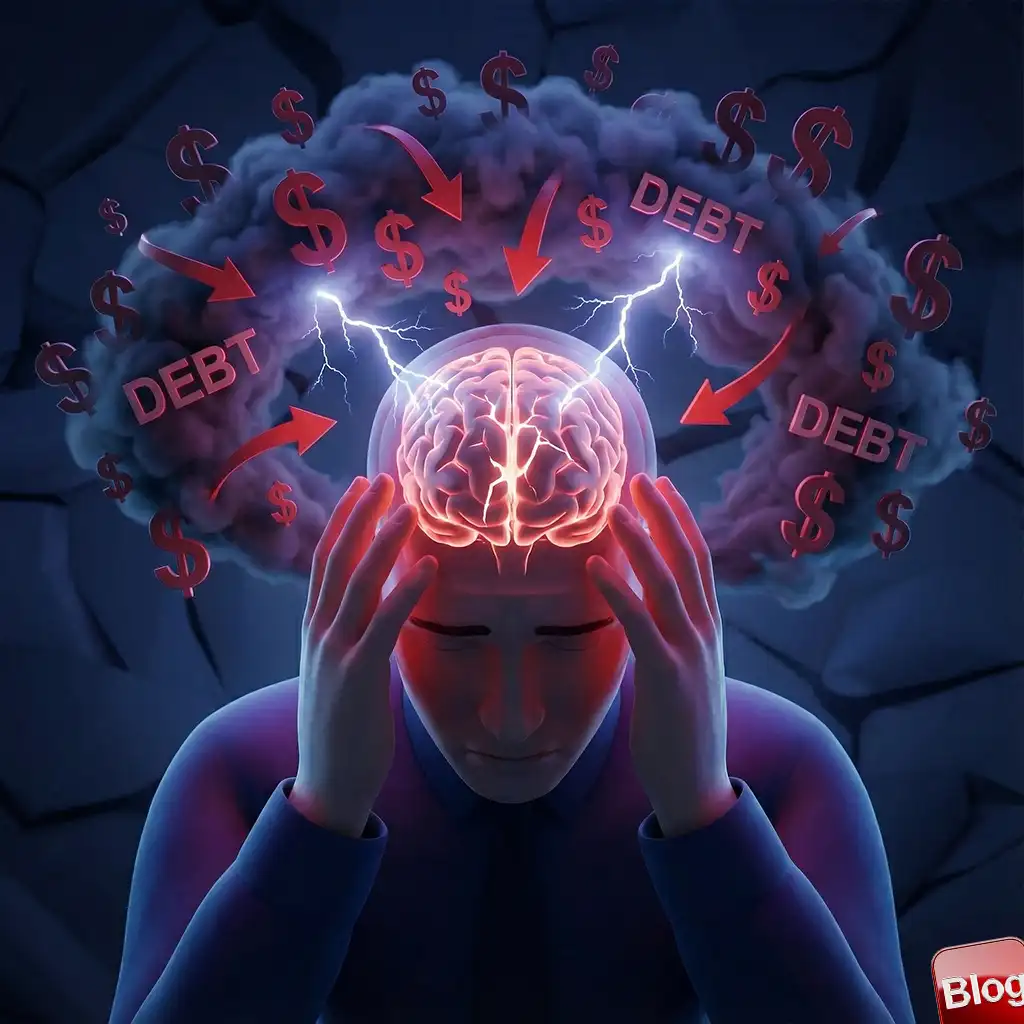

Mental Health and Decision Quality

Financial stress impairs cognitive function. Research published in Science demonstrated that financial worries consume mental bandwidth equivalent to losing 13 IQ points. Debtors delaying bankruptcy make decisions under this cognitive burden, often choosing poorly because their mental resources are depleted by constant financial anxiety.

Sleep deprivation compounds the problem. Collection calls, financial worry, and uncertain futures disrupt rest. Sleep-deprived decision-making produces worse outcomes across virtually every domain. The debtor considering whether to raid retirement accounts makes that choice while exhausted, anxious, and cognitively impaired—precisely the conditions most likely to produce poor decisions.

Filing bankruptcy often produces immediate psychological relief. The phone stops ringing. The mail becomes manageable. The future gains clarity. Debtors consistently report that the anticipation of bankruptcy felt worse than the reality. Mental health improvements begin the moment the petition is filed, not months later when discharge occurs.

Warning Signs That Delay Is Causing Damage

| Warning Sign | What It Means | Action Required |

|---|---|---|

| Using credit to pay credit | Cash flow crisis | Consult attorney immediately |

| Considering retirement withdrawal | Protected assets at risk | Stop and get legal advice |

| Receiving lawsuit papers | Judgment imminent | File before judgment enters |

| Wage garnishment started | Active financial bleeding | File to stop losses |

Calculating Your Personal Cost of Delay

Every debtor's situation differs, but calculating delay costs follows a consistent methodology. Start by identifying protected assets you might liquidate if you don't file soon. Add potential wage garnishment losses. Factor in interest accumulating on debts. Include attorney fees for defending lawsuits that bankruptcy would have stopped.

Monthly delay cost calculation steps:

- List protected assets you're considering liquidating and their full values including tax implications

- Calculate monthly garnishment amounts based on your income and existing judgments against you

- Add monthly interest accruing on all debts that would be discharged in bankruptcy

- Include stress-related costs like medical expenses, relationship counseling, or reduced work productivity

- Compare total monthly delay cost against bankruptcy filing fees and attorney costs

Most debtors discover that each month of delay costs more than the entire bankruptcy filing process. A $2,000 attorney fee seems expensive until you realize three months of delay costs $10,000 in garnishments, retirement account depletion, and interest accumulation. The math almost always favors filing sooner rather than later.

When Waiting Makes Sense

Strategic delay occasionally benefits debtors in specific circumstances. Waiting until income drops may help qualify for Chapter 7 rather than Chapter 13. Delaying to maximize available exemptions makes sense in states where longer residency produces better protection. Timing around tax refunds or expected windfalls requires careful planning. These situations require attorney guidance to navigate properly.

The critical difference involves purposeful waiting versus anxious avoidance. Strategic delay follows a specific timeline toward a defined goal. Anxious avoidance simply postpones the inevitable while assets erode and situations worsen. Most debtors who believe they're waiting strategically are actually just avoiding—and paying heavily for that avoidance.

Frequently Asked Questions

Will my credit score recover faster if I try to pay debts before filing?

No—the derogatory marks from late payments and collections damage credit regardless, and bankruptcy actually starts the recovery clock sooner than prolonged default.

Can creditors take my 401(k) if I don't file bankruptcy?

Creditors cannot directly seize ERISA-qualified retirement accounts, but you might voluntarily withdraw funds to pay bills—which bankruptcy would have prevented you from needing to do.

How do I know if I'm delaying too long?

If you're using credit cards to pay minimums on other cards, considering retirement withdrawals, or receiving lawsuit papers, delay has likely already cost you significantly.

Does waiting help avoid the stigma of bankruptcy?

Bankruptcy records are public but rarely searched by anyone except lenders, while the financial destruction from delay creates far more practical problems than any perceived stigma.

Should I use home equity to pay unsecured debts before considering bankruptcy?

Almost never—this converts protected exempt equity and dischargeable unsecured debt into secured debt against your home that cannot be discharged and could cost you your house.

What's the first step if I realize I've waited too long?

Consult a bankruptcy attorney immediately to stop further damage, as even if significant losses have occurred, filing now prevents additional erosion of your financial position.

Updated 2025-01-07